Finally, the works on your client’s home have been completed and they’re excited about moving in and looking forward to enjoying all the specialist adaptations that will make a big difference to their day to day living.

Finally, the works on your client’s home have been completed and they’re excited about moving in and looking forward to enjoying all the specialist adaptations that will make a big difference to their day to day living.

They’re now contemplating their next big financial decision and for some this may include the purchase of a second property, as either a holiday home or a buy-to-let. After all, there is a long history showing that residential property has delivered attractive returns.

However, I would hesitate caution for those who believe property is the “sure thing” for growing your client’s wealth.

There are several risks when you buy property directly, whether for clients or as a buy-to-let investment and these include:

-

Liquidity: Although you can sell the property if things get tough, the process is not as quick as it is to sell other investments such as shares.

-

Hidden and ongoing costs: Along with the initial costs of investing in property (i.e. stamp duty, legal and conveyance fees), you will need to consider the ongoing hidden costs of property investment such as fitting out the property, maintenance and repairs, building and landlord insurance, water rates, council rates, etc.

-

Rent free periods: There will be periods when you are unable to find a tenant and the property is vacant.

-

Bad tenants: Problematic tenants are every owner’s nightmare. They can severely damage your client’s property, refuse to make payments and sometimes even refuse to leave the property. Some disputes can take months to resolve and become very stressful, especially if there is an emotional attachment to the property.

For most people residential property will be their largest and most expensive asset and if you or your client is considering allocating more funds to this area, make sure you take expert advice from a professional who knows the market and understands your objectives.

But for some, the prospect of increased exposure to property will be unnerving and you will want to consider alternatives.

Unfortunately, for those who seek investment opportunities outside property the task can be even more daunting…..in the wrong hands the experience can be disastrous!

As you are aware many recipients of personal injury and medical negligence awards simply do not have the option to earn a living, and so managing their damages effectively is vital to their future wellbeing. Investing a lump sum and implementing a robust financial strategy can help them get the most from their award, so specialist independent financial advice is vital to protect your client’s interests.

And don’t be fooled by the complicated maths and confident opinions of our industry – there is not a single person in the world who knows what the market will do in the short term.

The most important question you need to ask yourself is, “How long am I investing for?” How you answer this question can change your perspective on everything.

When explaining investing to my eldest daughter who is beginning to show an interest in my chosen career path, I liken the investment markets to our family walk with our excitable dog, who’s darting randomly in every direction. Invariably, we set off on a Saturday morning walking through the park to the ice cream van (my youngest daughter only goes on a walk with the promise of an ice cream). At any one moment, there is no predicting which way the dog will lurch. But in the long run, we know that my youngest is heading towards the Mr Whippy sign and the direction the dog goes is incidental to her ambitions.

Investing for the long term is not dissimilar – focus on the goal and don’t be put off by market gyrations or the dog in this example.

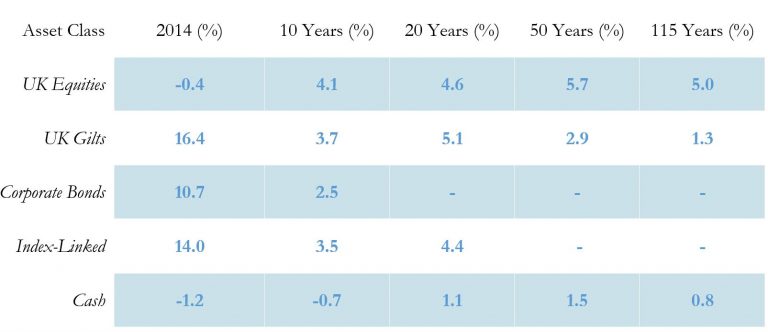

To put this into perspective, the table below shows the annualised real (i.e. after inflation) total returns from equities, bonds and cash over different time periods. I have chosen to use the UK markets for these purposes as there is an extremely comprehensive historical data set available.

The table illustrates that equities tend to provide significantly more attractive returns than both government bonds and cash over the long term. However, the risks associated with equities are higher and conservative investors will not want more than 40% of their portfolio allocated to this asset class:

At this point, it is worth mentioning that I believe we are in a low return environment and that future returns are likely to be lower than the historic averages.

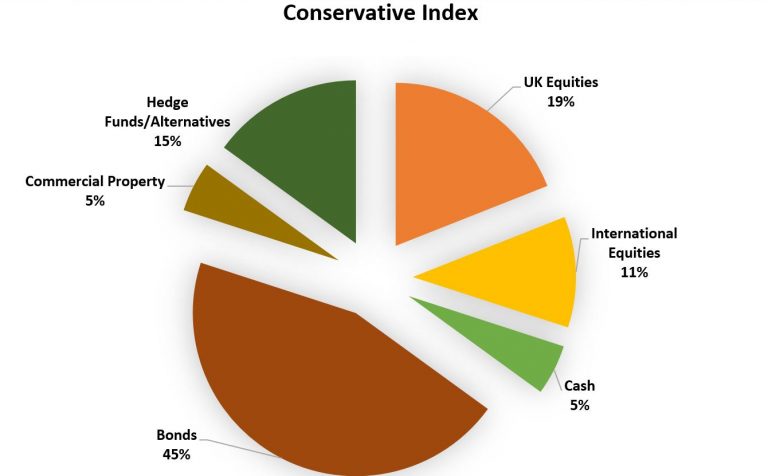

So, if residential property is not an option, as a conservative investor, how should your clients invest for the long term?

The Wealth Management Association (the representative body of the investment community) suggest the following allocation:

The above allocation is a good starting point but as you’d expect investment managers will formulate their own views.

Unfortunately, staying in cash is rarely an option and it is clear in today’s environment that investors need to protect their buying power against the eroding effect of inflation.

In most cases the Deputies or professional trustees give guidance to the client, ensuring the decision making process of deciding on the correct investment path is relevant to their client’s particular circumstances.

So, faced with a lump sum to invest and not knowing where to start, what questions should your client be asking a prospective investment manager?

The following may help you along the way:

-

Do you have your own money in the fund?

-

When was the last time your investment process failed?

-

In the event of another crisis, how much could I lose?

-

What do you own and why?

-

How will you benchmark your performance?

-

How much will I pay in total fees and costs each year?

The above questions will give you and your client a framework for the process and should help them make an informed decision on the proposals presented.

To end, I’d like to recall an article I read in the Financial Times “in 2008 the three most admired personalities in sport were probably Tiger Woods, Lance Armstrong and Oscar Pistorious”.

The same falls from grace happen in investing – chose your role models carefully!

Jonathan Fennell, Chartered MCSI

Partner

IPS Capital LLP

PLG Consultants